Dispelling myths about air freight exports

This article examines which goods contribute the most to air freight exports and what the outlook is for the availability of air freight capacity over the next couple of years.

Air freight is an important part of New Zealand exporters’ logistical infrastructure. Although only 0.3% of New Zealand’s exports by weight were freighted by air in 2014, these exports were typically more expensive items and, in value terms, accounted for 13% of the total value of New Zealand’s exports.

Time-to-market is a key factor that leads to the use of air freight for high-value items, either because clients demand urgent delivery of the goods, or because delays could bring the quality of the product into disrepute. Goods with a high propensity to be air-freighted are predominantly manufactured items and parts. Even though most agricultural products are sea freighted, the sheer scale of our primary sector means that even air freighting a small share of these goods adds up to significant number in value terms.

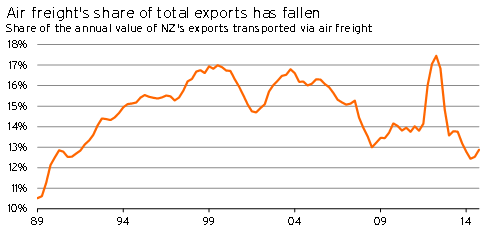

The share of exports dispatched via air freight peaked in the year to June 2012, but has since begun trending down again. The key reason for falls has been that the high New Zealand dollar has affected the competitiveness of some of our manufactured parts and seafood exports, while world prices for precious metals have eased over the past couple of years.

Graph 1.1

Studies also show that changes to fuel prices have a stronger effect on air freight costs than they do for sea freight costs1. As a result, the sustained period of elevated oil prices that lasted until mid-2014 will have caused some substitution towards slower sea-borne transportation for goods where there is flexibility surrounding time-to-market.

But with oil prices having plunged since late 2014 and now sitting at about half their June 2014 peak level, the competitiveness of air freight has improved once more. When one also considers that rising numbers of international flights are boosting air freight capacity, at a time when the New Zealand dollar has come off its peak levels against the US dollar, the outlook for air freight has brightened.

The remainder of this article decomposes the role of air freight for transporting New Zealand’s exports. We begin by considering the average value per kilogram of goods that are air freighted, as well as identifying which goods have higher propensities to be air freighted. The article then examines the outlook for air freight by considering both domestic and international trends in aviation connectivity.

How valuable are these air freighted exports?

In 2014, there was $6.7bn worth of goods exported using air freight, compared with $45.3bn using sea freight. The total weight of air freighted exports in 2014 was 104,753 tonnes – equivalent to 845 fully-laden 747-400 freighter aircraft. In comparison, the weight of sea freighted exports in 2014 equated to about 2,122 times the gross tonnage of the Aratere (Interislander) ferry (or 304,909 fully-laden 747-400 aircraft).

Using these insights, it is possible to calculate the underlying value of each kilogram of air and sea freight exports. Our calculations show that the free on board (i.e. excluding insurance and freight costs) underlying value of each kilogram of exports that was airfreighted in 2014 was $63.90/kg, compared with a mere $1.37/kg for goods that were sea freighted.

Given the high absolute cost of freighting goods via air, this significantly higher average value per kilogram of airfreighted goods comes as no surprise. Data from the New Zealand Productivity Commission2 shows that the cost of air freighting a kilogram of exports is close to 60 times more expensive than sending a kilogram of exports via bulk sea freight and around 34 times more expensive than containerised sea freight.

Which goods have the highest propensity to be exported using air freight?

Having established that air freight exports are typically of a relatively high value, it is interesting to look more specifically at the types of goods that are exported. This section will examine two dimensions of this problem.

- What proportion of total air freight exports does each type of export good represent?

- What is the propensity of each type of export good to use air freight?

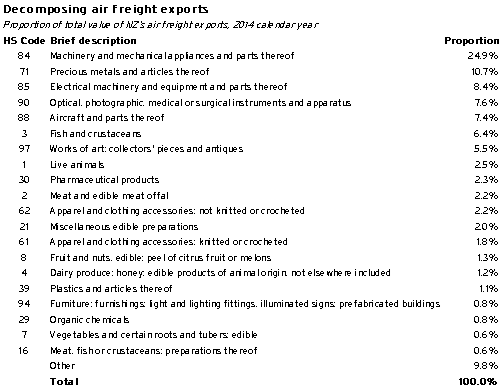

The first of these dimensions is essentially trying to find out what goods are the ones filling the holds of passenger aircraft and dedicated freight planes. Table 1.1 shows the top 20 most important contributors to the total value of air freighted exports during 2014.

With the exception of precious metals, the goods that contribute the highest amount to the total value of air freight exports are various types of manufactured goods, equipment, and parts. The next big contributor to air freight exports is the primary sector, with a range of dairy, meat, fish, and fruit/vegetable products helping fill the holds of outbound aircraft from New Zealand. Outside of these manufactured and primary sector goods, there are also important contributions from the arts and apparel sectors.

Table 1.1

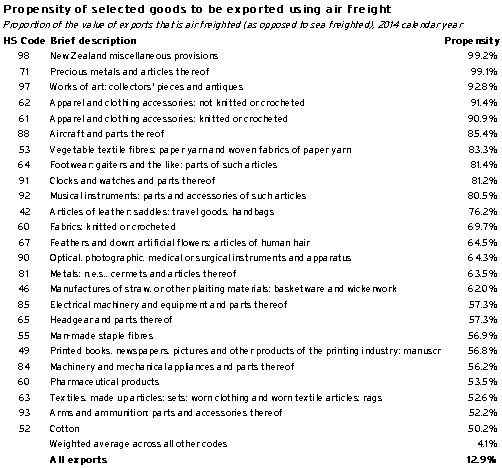

Having looked at what goods fill the holds of planes, it is useful to take a step back and look at the matter from another perspective. Table 1.2 shows the goods for which 50% or more of their annual earnings are derived from exporting via air freight (as opposed to exporting using sea freight). By considering the propensity of goods to be exported using air freight, we can get an idea of how vulnerable certain sectors are to trends in air freight costs and capacity.

Aside from miscellaneous provisions, there are three categories of goods for which more than 90% of exports are delivered using air freight. These categories are precious metals, art, and clothing. The fact that precious metals (mainly gold) and art have high propensities to be air freighted is understandable as buyers and sellers alike want to ensure that these high end items arrive swiftly and securely to their final destination. At first blush, it may seem strange that our clothing exporters rely so heavily on air freight, but keep in mind that these exporters are sending relatively small consignments to a widely dispersed global web of retailers – a situation that isn’t exactly conducive to the use of cheaper containerised sea freight.

The types of goods that have a 70-80% propensity to be exported via air freight are a mixed bunch and include fabrics, footwear, watches/clocks, hand bags and other leather items, musical instruments, and aircraft and aviation parts. Most of these items will use air freight for similar reasons to those outlined above for clothing. Aircraft exports are a bit unique in that some of these exports will almost certainly involve flying the actual plane that is being exported to its destination. In the case of aircraft parts, freight is typically best via air as it allows for speedy delivery – particularly in cases where an air operator overseas can’t get back into service before they receive the part.

There are a number of goods that have a 50-60% propensity to be exported, but rather than focusing on them all, let’s just examine the manufactured goods that fit this category, as we saw before that these are also the biggest contributors to the total value of air freighted exports. Table 1.2 shows that exporters of mechanical and electrical machinery, optical equipment and surgical devices, and parts of these items all rely on air freight to ship just over half of their exports. The need for air freighting is likely to stem from the demands of customers, who want their high value machine or part delivered quickly so that new systems can be commissioned or machines repaired in a timely manner. In these cases, it is worth paying a little extra for air freight, because any additional day that production is delayed is even costlier.

Table 1.2

Conspicuously absent from Table 1.2 are primary sector goods. This absence doesn’t mean that some niche products from the primary sector won’t have urgent time-to-market considerations, it is just that the data shows the majority of our primary produce can be sent in a more cost-effective manner via sea in chilled or frozen form. Furthermore, the large scale of our primary sector means that even a small share of the freight pie translates into a significant absolute value for primary sector air freight exports (see Table 1.1).

A surprising omission from both Table 1.1 and Table 1.2 is plant and fresh flower exports, particularly when proponents of air freight and regional air connectivity typically list fresh flower exports among those desperately needing such services. But while this capacity may matter for the individual grower, the data shows that the scale of this problem for the broader economy is overstated. Only 44% of plant and fresh flower exports are air freighted, and these exports only account for 0.4% of the total value of all air freight exports.

Looking to the outlook for air freight

Having examined which goods contribute the most to air freighters’ earnings, and which goods have the highest propensities to be air freighted, let’s delve into the outlook for air freight capacity.

Domestic connectivity

New Zealand exporters are fortunate that our nation has one of the best domestic air networks in the world, which is evident by the fact that almost everyone is within 1-2 hours’ drive of an airport with regular scheduled services. Given the geographically dispersed nature of our country and limited number of international airports, this domestic flight connectivity plays a pivotal role in connecting exporters in our regions with international air freight capacity at Auckland Airport (and, to a more limited extent, Christchurch Airport). The frequency of services is paramount in ensuring that time-sensitive exports can be quickly dispatched from our regions.

Exporters have benefited from a rising number of passenger flights on the domestic network over recent years, as freight is typically added to the holds of passenger aircraft. Our estimates show that domestic passenger numbers in 2014 rose 0.8%, and that growth has averaged 2.7%pa over the past three years.

The outlook for the number of domestic services over the next couple of years is good, as robust levels of economic activity will ensure that demand for passenger air services grows. Even a recent consolidation by Air New Zealand of the airports to which it flies domestically should not cause too many hassles. Not only has Air New Zealand lifted capacity and flight frequency at airports close to those where services were removed (typically within one hour’s drive), but smaller air operators are moving to re-establish many of the abandoned routes.

International air freight capacity expanding

Boom times for the tourism sector at present are good news for exporters reliant on international freight. The strong growth we are seeing in visitor arrivals from a variety of Asian, American, and European nations has seen airlines respond with significant increases to the frequency of flights and the range of direct international connections. Furthermore, this growth is expected to persist over the next couple of years at least.

When one adds to the mix the increased number of fuel-efficient new-generation aircraft in operating fleets, at a time when jet fuel prices have plunged, the outlook for international aviation at present is bullish. The upshot for exporters is that the level of international air freight capacity is expanding, and there is also likely to be some downward pressure on the price of air freighting each kilogram of exports.

Piggybacking off passenger aircraft services is also a more cost-effective way of getting additional freight out of the country than on dedicated air freighters. The logic is that passenger services are designed to earn their keep based on the number of passengers flying, with freight merely providing a bonus revenue stream for spare capacity in the hold of planes that are flying anyway.

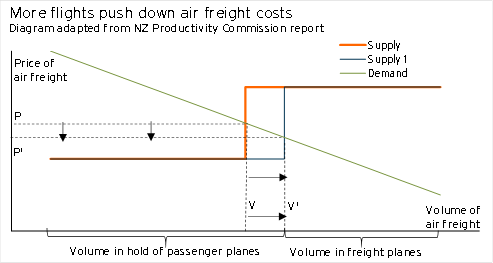

For those of you with some high school economics, a simple supply and demand diagram can help show theoretically how the rising number of passenger services could affect air freight pricing. Graph 1.2 is adapted from a diagram presented in the NZ Productivity Commission’s “International freight transport services inquiry” (April 2012).

Graph 1.2

The graph shows that supply essentially has two steps: lower-cost supply in passenger plane holds, and higher-cost supply on dedicated air freighters. The sharp lift in people wanting to visit New Zealand, and the ensuing lift in passenger services, has the effect of pushing out the supply curve from “Supply” to a new position at “Supply 1”. If you then overlay a downward sloping demand curve and look at its intersections with the old and new supply curves, you can observe that this outward movement theoretically puts downward pressure on the equilibrium price and upward pressure on the volume of air freight.

Conclusion

The overriding theme that comes out of the data is that air freight connectivity is far more than just a story of getting perishable primary sector goods to market. In fact, the majority of air freighted exports from New Zealand are actually high-value manufactured goods. Customers for these types of goods don’t want to wait for their order, as every day of downtime is costing them. Air freight enables our manufactured goods exporters to better connect with markets and provide reliable and rapid service to globally dispersed customers.

In order to keep this logistical framework running smoothly, it is important that regular international air services are available to a range of areas of the globe. Fortunately for exporters, the prognosis for this air freight infrastructure over the next couple of years is good. With demand for tourism to New Zealand booming, at a time when fuel operating expenses for airlines have plunged, many airlines are increasing their long-haul services to New Zealand. These additional services mean that the volume of cost-effective air freight capacity in the hold of passenger planes is growing.

1 For example, see David Hummels report, “Globalisation and freight transport costs in maritime shipping and aviation”.

2 “International freight transport services inquiry” (April 2012), NZ Productivity Commission