Decomposing domestic trends in road, rail, and sea transportation

This article covers trends in the domestic transportation of freight over recent years. The majority of freight in New Zealand is carried by road with smaller, but not insignificant, quantities carried via rail and coastal shipping. According to the Ministry of Transport’s 2008 National Freight Demands Study, about 70% of freight tonne-kilometres were shifted by road, while the remainder of freight was carried approximately equally by rail and coastal shipping.

Freight transportation activity appears to have increased significantly over the first half of 2013, as rising domestic economic activity and elevated primary production pushed up demand for freight forwarding and the transportation of imports and exports. Coastal shipping activity increased the most rapidly, while rail activity also rose modestly – despite a significant decrease in coal volumes. Road transportation activity was subdued during the first half of 2013, but has recently picked up more rapidly.

It appears that price-setting power for road transport operators improved over the year to June, with output prices for the road transportation industry rising a moderate 2.5%, while output prices for other types of transport (rail, water, air) eased 0.4%. Input cost pressures across all types of transport operators remain constrained according to the producers price index, with input prices for the road transport industry climbing a mere 0.1% over the past year, while over the same period other transport input costs fell 0.1%.

The remainder of this article decomposes these broader trends in freight haulage by taking a closer look at road, rail, and coastal shipping activity levels.

Road transportation activity showing signs of an acceleration

Assessing activity levels in the road transportation industry has been difficult over the past year. We usually focus on RUC kilometre purchases as our primary road transport activity indicator, but changes to the RUC system in August 2012 affected purchasing incentives across truck weight classes, causing a break in the data. We expect to be able to begin making interpretations again from RUC data by the end of this year. In the meantime, we are looking at diesel sales data and ANZ’s heavy vehicle index as indicators of road transport activity.

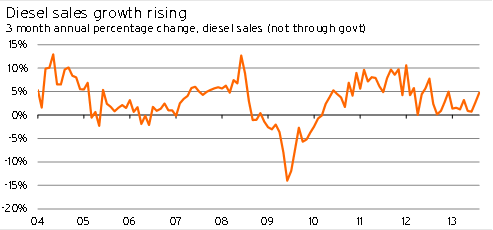

ANZ’s heavy vehicle index comprises flows of vehicles weighing more than 3.5 tonnes at 11 selected roads around New Zealand. According to the index, heavy vehicle activity in June was 1.1% below its level from a year earlier. However, over the past couple of months trucking activity has strengthened, with activity levels in September sitting 8.1% above their September 2012 level. Diesel sales data tells a similar story, with non-governmental diesel sales growing by a mere 0.7% in the June quarter from a year earlier, before growth accelerated to 4.7%pa for the three months to August.

The recent lift in heavy traffic flows and diesel sales is consistent with the broad-based pick-up we have seen in other economic indicators over the past couple of months. With economic activity accelerating, we anticipate that road transport activity will continue rising in 2014. Increasing sales of medium and very heavy trucks also shows that the industry has confidence in the outlook for road transportation activity.

Graph 5.1

Rail activity rises, despite falling coal production

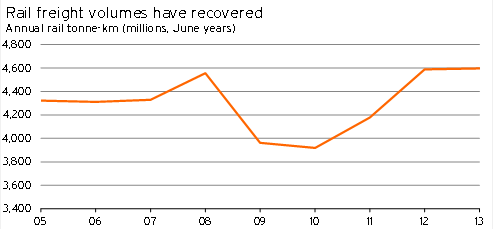

Over the year to June 2013, rail freight tonne-kilometres (RTKs) rose 0.2% from a year earlier1. However, this increase would have been even greater had it not been for an 8.7% drop in coal transportation volumes. Excluding coal, RTKs would have risen by 2.6%.

This increase in rail freight activity marks the continuation of a recovery that began in 2011, following a sharp plunge in 2009/10 when the Global Financial Crisis and domestic recession led to lower freight volumes of coal and general imports and exports, as well as significantly less freight forwarding. RTKs now sit 0.9% above their 2008 peak.

Graph 5.2

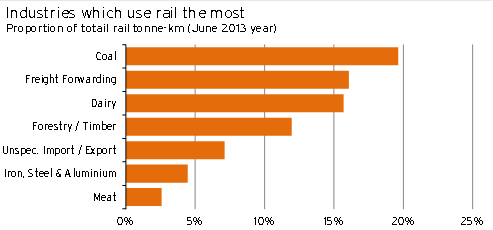

Although rail only accounts for around one quarter of the number of freight tonne-kilometres carried by the road transportation industry, rail is an important carrier of key export commodities such as coal, dairy, and logs. Many Fonterra dairy factories have been strategically built on main trunk lines to streamline access to port facilities, while trains are also an efficient way of transporting heavy loads of coal and unprocessed logs to ports. Graph 5.3 identifies the industries that used rail the most over the year to June 2013.

Graph 5.3

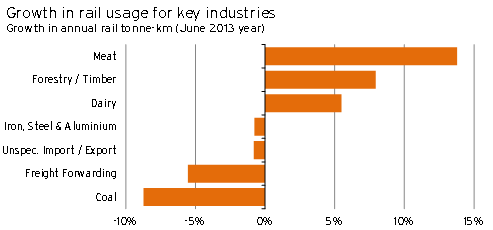

Of these key industries, there has recently been significant divergence between growth rates of rail usage (see Graph 5.4). Annual RTKs for meat, forestry, and dairy all grew strongly over the past year, which is consistent with increases in exports of these products. Coal volumes have fallen significantly over the last year, as underlying coal production has eased in response to plunging coal prices.

Graph 5.4

Over the coming year, we anticipate that coal volumes will come under further downward pressure, while meat volumes will fall as production has settled at a lower level following the drought. However, this weakness will be more than offset by rising exports of forestry products, elevated dairy production, and rapidly improving demand for imported goods. As a result, RTKs should continue their upward march during 2014.

Coastal shipping shrugs off industrial dispute at Port of Auckland

Over the six months to June 2013, freight tonnes carried by coastal shipping were 8.9% above their level from a year earlier2. Although underlying economic activity has picked up significantly during 2013, coastal shipping a year earlier was held back by industrial action at Auckland’s port. Of the major ports, freight movements through the ports of Auckland, Tauranga, and Lyttelton rose (up 47%, 23%, and 57% respectively), while freight tonnes carried through the ports of Napier and Nelson fell (down 2.7% and 25% respectively).

Over the past year, domestic goods accounted for 38% of total freight tonnes carted by coastal shipping, while 52% was transhipment movements of goods for export, 9.5% was the transhipment of imports, and 1.0% was unknown.

Although coastal shipping only moved 13% of the volume of freight tonnes that rail carried during the June 2013 year, the distances travelled by coastal shipping are typically a lot further. Coastal shipping is efficient for freight journeys between the islands as it removes the need for rail carriages to be shunted onto Cook Strait ferries. Around 65% of freight movements by coastal shipping involved shifting goods between the ports of Auckland or Tauranga and South Island ports. By comparison, only around 3.5% of the freight tonnes carried by rail involved movements between Auckland/Waikato/BOP and South Island locations. As a result, rail and coastal shipping’s shares of freight haulage are likely to have been closer on a freight tonne-kilometre basis. This assertion fits with the Ministry of Transport’s 2008 National Freight Demands Study, which showed that rail and coastal shipping had approximately equal shares of freight tonne-kilometres in the domestic transport industry during the June 2007 year.

With coastal shipping journeys always needing a land transport component at either end, it is also important to consider the interplay between the shipping industry and road and rail transportation. The majority of land transport to and from ports is by road, with 67% of goods arriving at port by road over the year to June 2013, while 73% of goods left port by road over the same period. In contrast, 31% of goods were delivered to port via rail, whereas 25% of goods left ports using rail. These figures highlight the important role played by rail in getting key agricultural and mineral commodities to ports for export, while the road transportation industry is especially crucial for collecting goods from ports and delivering them to locations away from main trunk lines.

Graph 5.5

The outlook

Over the coming years, we anticipate that rising domestic activity and elevated primary production will continue to push up demand for domestic freight transportation. The transport-intensive nature of rebuilding work in Canterbury and home building in Auckland is likely to push up road transport relatively rapidly, while rising export volumes will also ensure that rail and coastal shipping activity levels continue to increase.

In the longer-term, the government’s policy direction will play a key role in the balance between the various domestic freight transportation methods. On one hand, the government has expressed a desire to grow coastal shipping’s share of freight movements, while on the other, the building of Roads of National Significance and KiwiRail’s revival favour land transportation.

Another key factor that could influence the outlook is the proposal to move the Cook Strait ferry terminal to Clifford Bay. If the terminal is indeed moved, then Clifford Bay’s strategic location would drive efficiency gains for interisland movements of freight via rail and road, which could tip the balance further in favour of land transportation options.