Where has the floor on oil prices gone?

Although we had been forecasting an easing in fuel costs during the second half of 2014 and into 2015, the magnitude of the decline has taken us, and other analysts, by surprise. Oil costs are important for both business activity and households, and this article will discuss why oil prices have fallen, and what we expect to occur going forward.

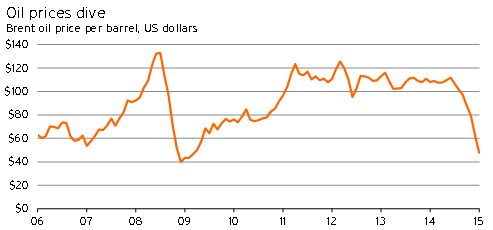

With global oil supplies surging during 2013 and throughout 2014, it was clear that the worst of the oil price spikes were behind us. However, it was also believed that the cost of extracting shale oil from the United States would provide a floor for prices, as higher-cost production from these fields was the additional output required to meet global demand. Given this assumption, we wouldn’t have expected the price of oil to fall much below US$80/bl – a price at which around 25% of shale fields in the US are uneconomical. However, prices slipped below US$50/bl in mid-January.

Although Brent oil prices have recovered to US$60/bl as of this article going to print, they remain well below their previously assumed floor.

So is the sharp decline in oil prices a good or a bad thing for New Zealand? At first glance, it is easy to think cheaper prices at the petrol pump is only a positive. But the last time we saw a big fall in oil prices was at the beginning of the Global Financial Crisis – a crisis whose negative effects continue to plague us to this day.

To get to the bottom of what has happened to the price of oil and what the outlook for prices is, we must decompose the situation into its underlying root causes. We can group the causes into four categories: a weaker world economy, higher supply, the rise of oil substitutes, and competition and geo-politics. We’ll discuss these categories in detail below.

Graph 5.1

The four causes

Lower demand from a weaker world economy

The first factor to consider regarding falling oil prices has been a stumbling global economy, which has also been reflected in downward revisions to global growth for 2015.

Slower growth in the global economy won’t just reduce the price of oil, but will also lead to weaker demand for the goods and services that New Zealanders sell overseas. This weaker demand would reduce prices for agricultural and manufacturing products and lead to fewer tourist arrivals. In this way, lower oil prices are a symptom of a weaker economic outlook – and as a result can be seen as a negative thing.

Both OPEC and the International Energy Agency (IEA) revised down their forecasts of global oil demand for the 2015 year during the last quarter of 2014.

Part of the reason for the sharp decline in oil prices after OPEC’s monthly report in December was the nature of the decline in oil demand that it (and the IEA) was forecasting. OPEC was forecasting lower demand from the OECD to be the primary driver of weakening global demand – even though the key negative surprises to date had been in emerging markets. As a result, there was an expectation that OPEC would lower its demand forecasts further, which it did in in January.

A core concern has been that the recent slowdown in economic growth in China and other developing economies will be persistent. With developing countries having driven growth in the global economy in recent years, the expected slowdown has filtered into all commodity prices, including oil.

Demand for oil is very inelastic at any given point in time – in other words, the amount that people want to buy doesn’t change very much when the price changes. Global supply is also inelastic, so it only requires a relatively small shift in global demand for oil for there to be a big price response.

However, it is misleading to view the drop in prices as primarily the result of a weaker global economy – the current situation is very different to 2008. In a piece from VoxEU1, economists Rabah Arezki and Olivier Blanchard look at the elasticity of supply and demand for oil. They point out that lower demand accounts for only 20-35% of the recent drop in prices – and as we will discuss later, much of this lower demand is not due to weaker economic growth. A similar point has also been made by Goldman Sachs economists2. As a result, we need to explore other factors to understand what is going on.

Higher supply

Although lower demand due to weakness in the world economy is very important, it is not the sole driver of lower oil prices – unlike the price crash during 2008/09.

The prior piece from VoxEU noted that there has been a significant disjoint between movements in the price of metals and the price of oil since the middle of 2014.

A greater supply of oil in the world is an undeniably positive thing for a net oil-importing country like New Zealand. Oil is an input into production for a large number of New Zealand firms, and lower oil prices imply lower transport costs to most New Zealanders.

There are some potential losers – those that benefit from oil extraction in Taranaki, and potentially New Zealand farmers if the cut in costs for their more oil-intensive competitors overseas leads to lower dairy and meat prices. However, in net terms a drop in oil prices, based on higher global supply, is a good thing for New Zealand.

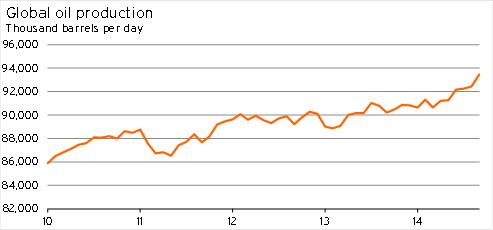

The supply of oil has risen sizably over the past year after several years of virtually flat lining, with production in September 2014 up 3.6% from a year earlier.

Graph 5.2

The lift in oil production in the United States and Canada has been the key driver of higher global supply. A 13% lift in Canadian production and an 11% lift in US production were behind over half of the increase in global production between September 2013 and September 2014.

The surge in oil supply from the US and Canada has largely been due to fracking, which has allowed the extraction of oil from shale reserves. After years of investing in extraction infrastructure, North America now has the capability to produce a significant amount of oil from these reserves. However, these increases in production are coming from a relatively expensive source3. As a result, the increase in supply is unlikely to last if oil prices remain as low as they are.

Also helping to boost overall US supply has been better weather conditions in the Gulf of Mexico. There have been no major hurricanes in the Gulf of Mexico recently, and there has also been sufficient water to allow continued production (something that hasn’t been the case in the US in recent years due to drought).

Outside of the United States, another positive for oil production has been a sharp boost in output in Libya and Iraq, while output in Syria had been continuing unabated. Between September 2013 and September 2014, production from Libya rose 104%, and production from Iraq increased 24%.

The supply situation in these Middle East countries seems a little surprising at first glance, given that all these countries are currently embroiled in civil wars and, in the case of Iraq and Syria, much of the conflict is taking place near oil production fields.

The Libyan revolt had begun in May 2014, and ISIL4 took Mosul in June 2014. As a result, in June when these respective civil wars were intensifying and oil prices were high, many analysts expected them to head even higher (with instability in Ukraine also playing a role). However, production rose and prices fell instead.

One of the big reasons for this is that oil production remained in the hands of organised groups, who were interested in continuing to produce and sell oil. As a result, the only interruption to supply would occur when oil fields and production and transportation infrastructure were destroyed.

In the later stages of 2014, oil production in Libya and Iraq-Syria both started to move backwards, as oil related facilities were destroyed. By December 29, the US claimed that they had “debilitated ISIL's oil producing, processing and transportation infrastructure”. As a result, the boost in supply from these regions that took place during 2014 looks likely to fall away in 2015.

Having run through the different ways that supply was boosted during 2014, these factors seem to provide a compelling reason why prices trended down for much of 2014. However, on the face of it, the gradual lift in supply doesn’t explain the sudden drop in oil prices since November.

However, it is important to keep in mind that crude oil can be stored. In the face of an imbalance between supply and demand, for a given price at a point in time, the remaining crude oil can be held as inventory. Rising production had ensured that, by September, storage had built up – with rising sea storage a sign of oversupply5.

As Blanchard and Arezki note in somewhat technical terms:

The steady increase in global oil production could be seen as ‘the dog that didn’t bark’. In other words, oil prices had stayed relatively high in spite of the upward trajectory in global oil production due to the perception at the time of OPEC’s induced floor price. The resulting shift by the swing producer [Saudi Arabia], however, helped trigger a fundamental change in expectations about the future path of global oil supply, in turn explaining both the timing and the magnitude of the fall in oil prices, and bringing the latter closer to the level of a competitive market equilibrium.

In other words, people had been pricing oil (as a durable product) based on expectations about future production. Once it became clear that future production would be higher than expected, prices slumped.

However, a key fact is that the price of oil is currently below the cost of production for a vast number of fields. For example, if prices were to fall below US$40/bl, it would cost all Russian oil fields more to extract and produce oil than they would get for selling it.

In this way, the current level of supply does not seem sustainable, implying that something will have to give. Either costly producers (such as North American shale production) will go out of business, or OPEC will need to cut production. So the drop in oil prices due to current supply is likely to eventually cease being a key contributor to the situation.

Substitutes

Another factor that is reducing demand for oil, by increasing the supply of energy relative to the need for energy, is rising energy efficiency and the growing affordability of substitutes to oil.

Cheaper substitutes and rising energy efficiency are both ways that demand for oil can fall, without a corresponding drop in global economic activity. As far as this factor is a driver of lower oil prices, it is a good thing for New Zealand – just like in the case where supply has risen.

However, technology that creates substitutes to oil is an even more positive outcome for New Zealand than greater oil supply. Oil is a non-renewable resource, so higher supply leads to a temporary dip in prices, while rising numbers of substitutes leads to a permanent dip.

The key substitutes in recent years have been natural gas, coal, and the rise of renewable energy. Although the former two are also finite resources, the latter, by definition, will not be exhausted.

As part of the fracking revolution in the United States there has been a corresponding lift in natural gas production – given that it is a side product of the process.

For many forms of energy generation coal is a cheaper, and more abundant, substitute for oil. By 2014 coal had overtaken oil as the largest source of gross energy production globally. However, coal prices have been moving in step with oil as they are subject to the same concerns – the fear of peak coal, and the growing supply of renewable energy as a substitute.

Non-hydro renewable energy generation has increased significantly in recent years, with government subsidies and investment combining with high oil prices to provide a strong incentive for investment. By 2014, non-hydro renewable energy accounted for 11% of all gross energy production globally6 – more than hydro-dams and nuclear power combined! This lift has largely been due to a phenomenal rise in wind and solar power generation in the past decade7. Furthermore, 21% of global electricity production in 2011 was from renewable sources (including hydro-dams).

The EIA expects the importance of renewable generation to continue rising, accounting for a quarter of electricity production and 15% of total energy consumption by 2040.

Even this forecast could be conservative given the step-change in cost-effectiveness occurring with solar energy. At present, solar power only counts for a small percentage of overall energy production, but 2014 represented the first year where solar started to look cost-effective on a broad scale8. The sudden cost-effectiveness of electricity generation by solar will produce a downward adjustment in the price of other sources of energy, although the timing of this step-change is difficult to predict. It is possible this step-change is occurring now, but the lack of data indicating that a monumental surge in solar investment has occurred suggests this factor is more likely to be a reason why oil prices will not recover sharply, rather than a driver of the recent fall.

At the same time as there has been a proliferation of cost-effective alternative forms of energy, increasing energy efficiency has also helped reduce demand for other forms of energy.

High oil prices have provided an incentive for researchers and firms to focus on improving the energy efficiency of the devices they create. Furthermore, the introduction of reverse metering and clearer market pricing for power has led to a situation where consumers demand greater levels of energy efficiency from their devices.

This process is most clearly shown in US data9, with 8.8% less energy used per unit of GDP in 2013 than in 2007, and 18% less used than in 2001.

Rising numbers of substitutes and growing energy efficiency have reduced the negative effect of high oil prices on the New Zealand economy in recent years, and also indicate that at least part of the recent drop in prices will be permanent.

Competition and geo-political posturing

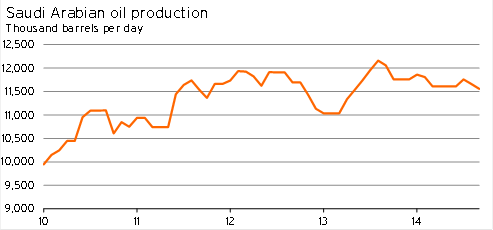

As the main producer among OPEC, Saudi Arabia strongly dictates where global oil prices go with the production levels it sets. Due to this, Saudi Arabia is termed the “swing producer” of oil.

There has been a lot of chatter suggesting that Saudi Arabia is more than happy to let crude oil prices slump right now, as it will drive the high-cost shale producers in the US out of business. This type of behaviour is called predatory pricing – and it is one of the most commonly confused concepts in economics, especially by European governments.

If Saudi Arabia is genuinely interested in knocking out US shale producers, then it implies that allowing oil prices to sit above US$100/bl since early 2011 was a mistake. However, given that this level of oil prices is required by the Saudi Arabian government to balance the books, we think the predatory pricing argument is being oversold.

Instead, Saudi Arabia’s decision may be geo-politically motivated, with suggestions that it is trying to undermine Russia10 and ISIL by allowing the price of oil exports from these countries to plummet.

However, what is likely to be even more important for Saudi Arabia is the conflict within OPEC. The Saudis are keen for other oil producers to vary their output more when trying to maintain high oil prices in the future.

It is important to note that Saudi Arabia had already cut production significantly prior to oil prices slumping – production in September 2014 was down 4.1% from September 2013. Given that Saudi Arabia produces over 12% of all crude oil, this cut was a significant one. If production had not been cut, global production would have been up 4.1% from September 2013 (instead of the 3.6% it actually rose).

As the “swing producer”, Saudi Arabia has to cut back production to keep prices high, thereby sacrificing income in order to benefit other oil producers. Although it had appeared that there was more scope for Saudi Arabia to cut production, it seems to have decided enough is enough, and is now determined to protect its own market share.

Graph 5.3

An internal battle within OPEC is likely to be a major factor behind the magnitude of the decline in oil prices, mirroring the drop in oil prices experienced in the early 2000s.

The outlook

Any outlook for oil prices depends strongly on which of the above causes we view as the most important, and how permanent we expect the effects of that cause to be on prices.

As has been seen during February, any indicator that US supply is falling has been taken as an important sign that higher prices may be necessary. The sharp drop in US drilling rigs currently in action is a large part of the reason for the rally in oil prices in the past month11.

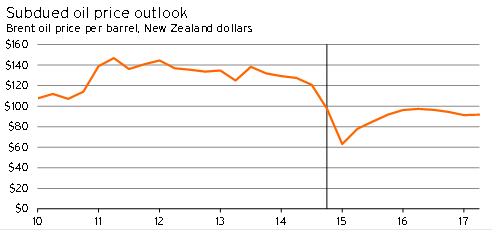

The important role of US supply would suggest that the current low level of oil prices is unsustainable, and once US production has adjusted we can expect prices to slowly rise. The magnitude and timing of these increases will be delayed by how long it takes to run down the oil inventories from their currently elevated level.

Graph 5.4

Although we expect oil prices to recover to US$65/bl during 2015, we do not expect the price to rise above US$70/bl again during our forecast period (until June 2017). At this level, investment in shale capacity in the United States is expected to have pulled back significantly, while broader global economic growth will also have recovered.

We do not expect oil prices to return to levels above US$100/bl during the forecast period, with the increasing cost-effectiveness of energy substitutes putting a cap on how far prices will rise. Unlike the 1970s, global economies have a much more diversified set of methods for extracting and generating energy – a factor that makes the price of oil less and less important as time goes on.

1 www.voxeu.org/article/2014-oil-price-slump-seven-key-questions

2 www.bloomberg.com/news/articles/2015-02-11/goldman-here-s-why-oil-crashed-and-why-lower-prices-are-here-to-stay

3 www.econbrowser.com/archives/2014/11/a-glut-of-oil

4 ISIL, or the Islamic State of Iraq and Levant, is more commonly referred to ISIS (Islamic State of Iraq and Syria) in New Zealand media. However, many of the American organisations we are quoting in this article prefer to refer to the group as ISIL, and we have followed that convention here.

5 www.oilprice.com/Energy/Crude-Oil/Dropping-Prices-and-Supply-Glut-Sends-Oil-Into-Floating-Storage-At-Sea.html

7 www.iea.org/aboutus/faqs/renewableenergy/

8 www.bloomberg.com/news/articles/2014-10-29/while-you-were-getting-worked-up-over-oil-prices-this-just-happened-to-solar

9 www.eia.gov/totalenergy/data/monthly/pdf/sec1_16.pdf

10 www.businessinsider.com.au/saudi-arabias-political-play-in-oil-2014-12

11 www.marketwatch.com/story/oil-prices-volatile-after-weak-china-trade-data-rig-count-drop-2015-02-09 and www.bloomberg.com/news/articles/2015-02-13/number-of-u-s-oil-rigs-continue-to-tumble