The return of the American house

After a long malaise, there is talk that the US housing market is rebounding. Here we sift through the evidence, give our interpretation about where the US housing market is, and look at where it may be heading.

The US housing market played a key role in the lead-up to the Global Financial Crisis, and was a key driver of the length of the GFC. The global financial system had been inextricably linked to the outlook for house price growth in the United States due to the repackaging of subprime mortgage loans and the sale of these repackaged bonds around the world. As a result, the US housing market has taken on a disproportionately important role in determining the global economic outlook. Not only is the US housing market a driver of growth in demand in the US economy, but it is also a key driver of confidence in broader financial markets.

In this article, we will take a look at what has been happening in the US housing market recently, and where it will head over the next couple of years.

Sales and inventories

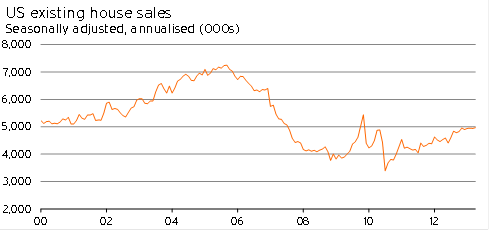

House sales in the United States have recovered significantly from their late-2010 lows. In April, house sales were up 9.7% from a year earlier to their third-highest level since July 2007 (seasonally adjusted).

Graph Error! No text of specified style in document..1

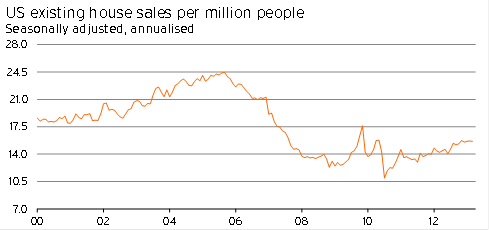

Although this increase in sales is nothing to sneeze at, house sales are still down 5.8% from their decade-long average. Furthermore, if we were to look at house sales per capita, activity remains 11% below its decade-long average.

Although it is undeniable that lower interest rates, rising consumer confidence, and easier credit availability are boosting house sales in the US, underlying activity is still at a low level Credit availability for households who have low credit ratings is especially acute1.

Graph Error! No text of specified style in document..2

People are also becoming more unwilling to sell

However, house sales only tell us part of the story. Low sale numbers may not be the result of people unwilling to buy, but instead the result of people unwilling to sell.

The inventory figures in the US suggest that the stock of housing available for sale on the market is indeed low. At current levels, there is only 4.1 months’ of stock on the market. At this level, inventories relative to sales are at a similar level to those recorded prior to the bubble bursting in 2005, but inventories are well below their historic average.

Graph Error! No text of specified style in document..3

Distressed sales are harder to get a handle on, given that there isn’t a single central measure of these types of sales. However, reports from realtors suggest that distressed sales are well down from a year earlier (with reports of distressed sales falling 25% common2).

Part of the reason house sales spiked up during 2009 in the United States was the prevalence of distressed sales. In this regard, the fact that overall house sales are rising while distressed sales numbers are slumping is a strong positive sign for the US housing market as a whole.

The Federal Reserve has been clear that it believes current sales and building levels are unsustainably low, and are only being maintained due to a willingness by households to boost occupancy rates and keep the number of people per dwelling at a higher level. Even so, the lift in the average number of people per household has not been as stark in the US as it has been in New Zealand, and according to the US Census bureau, the number of people per dwelling started to decline again during 2012.

Pushing up prices

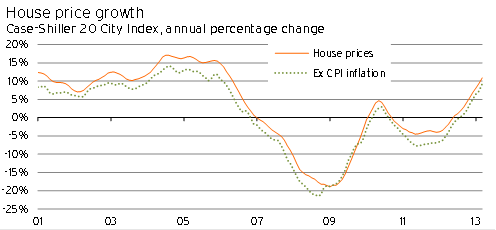

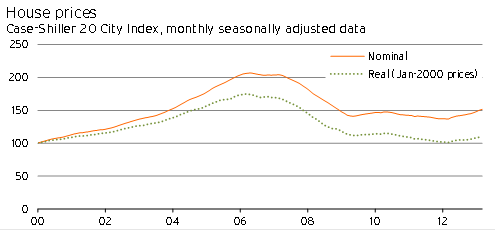

Although sales numbers remain relatively low, the drop in inventory and reduction in distressed sales has led to house prices recovering.

Graph Error! No text of specified style in document..4

Graph Error! No text of specified style in document..5

The return of double-digit house price growth is an encouraging sign that life is returning to the US housing market. However, at the moment, this growth simply represents the fact that distressed sales have ceased. Underlying real house prices are barely above their level at the start of the millennium.

Households’ willingness to spend up large on housing is still being constrained by uncertainty about the economy, the significant drop in real median incomes experienced over the last 15 years in the US, and a recognition that house prices can fall! As a result, it will take further improvement in the labour market to combine with the current incredibly low mortgage rates for house prices in the US to keep growing at current rates.

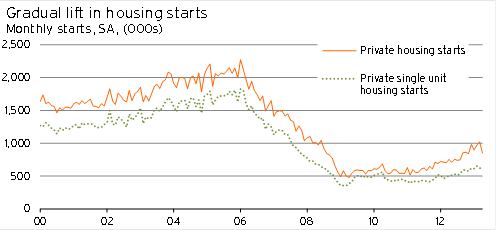

How is building responding?

With house prices rising again, and financial conditions improving, there should be a lift in residential building activity.

And this is exactly what has happened. In the year to April, private housing starts have risen by 29%, with the less variable single-unit housing starts figure climbing 26%.

Graph Error! No text of specified style in document..6

Graph Error! No text of specified style in document..7

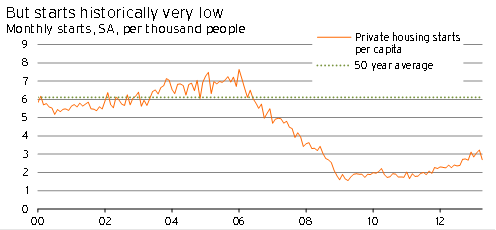

Even with the recent strong lift in building starts, activity remains at a very low level.

Ever since the US housing market started to stall in 2006, build rates have dropped below their 50-year average. With current and expected population growth both lower than they have been in the past, the build rate should be below this historical average. The fact that the build rate was previously at such a high level indicates the amount of overbuilding that took place in the United States.

At around three housing starts for every 1,000 people, and with the issue of oversupply having been worked through in many states, the build rate is currently too low. Given current population growth estimates, a build rate of around 4.2 houses per 1,000 people is believed to be closer to “normal” conditions for the US housing market.

As a result, even though building activity has recovered by about 50% from its lows, it could experience a further 25% lift before building activity would be back within a “normal” range.

The outlook

Although there has been a lot of talk in the media about the drastic recovery in the US housing market, when the figures are put in a historical context, the US housing market is still incredibly weak.

The lifts in house sales, prices, and construction activity during the past year appear to be the result of households not being in distress anymore, rather than an indication that households are keen to invest in housing again. This outcome suggests two things.

· The housing market is recovering, but not roaring to life, implying that the feedback into GDP will be modest.

· There is significant scope for further growth in residential building activity in the US.

The fact that activity remains historically low, and consumers and banks in the US are still nervous about the housing market, has led us to be cautious with our forecast for US economic growth in the coming years. However, given there is so much scope for residential building work to recover, there is a significant risk that a sharper pick-up in construction could feed through into stronger economic growth.