Adding value in the timber industry is not easy

Although log exports are booming, wood manufacturers are going through tough times. This article explores the reasons for these diverging fortunes and examines what can be done to help the wood processing industry.

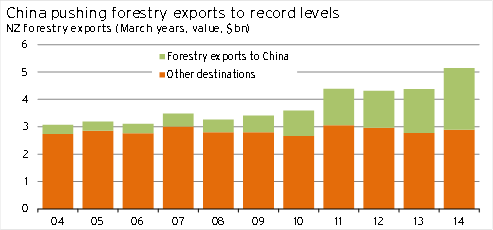

Forestry exports from New Zealand have soared to record levels over the past year, pushed up by exceptional growth in demand from China. Over the year to March 2014, the value of forestry exports rose by 18% to a record $5.2bn, with 84% of this lift in forestry export earnings derived from China. Growth in Chinese purchases of New Zealand forestry products has been fuelled by a combination of rising underlying demand and constrained domestic supply, as Chinese authorities continue to increase their efforts to protect the environment.

Chinese demand has also accounted for virtually all of the New Zealand forestry industry’s export growth over the past decade. The annual value of New Zealand’s forestry exports rose two thirds between March 2004 and March 2014, but if we exclude China from the mix, annual forestry exports to all other nations grew by just 5.5% over the same period.

Graph 5.14

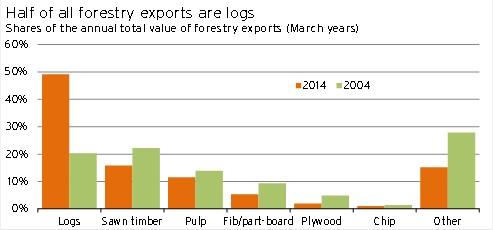

The rise of China as a key buyer of New Zealand’s forestry exports has led to a dramatic change in the composition of the types of forestry products sold. Although traditional forestry trade partners such as Australia, the US, Korea, and Japan purchase significant quantities of sawn timber and manufactured wood products, the overwhelming majority of the value of forestry exports to China (some 82%) comes solely from the sale of unprocessed logs. As a result, logs now account for approximately half of all New Zealand’s forestry export receipts – up from 20% a decade ago.

Unsurprisingly, with more and more forestry exports leaving New Zealand as unprocessed logs instead of being processed domestically, there has been a significant squeezing of the wood processing industry. Between March 2004 and December 2013, the size of New Zealand’s annual forestry harvest grew by an average of 3.7%pa. In the March 2004 year, 65% of this harvest was processed domestically, but by the end of 2013, this share had fallen to 45%.

Putting things in terms of economic growth, we estimate that the wood product manufacturing industry’s GDP fell by an average of 0.8%pa over the ten years to March 2013.1 Over the same period, forestry and logging, and forest support services GDP rose by 1.9%pa and 0.5%pa respectively as a result of increases to the size of the underlying forestry harvest.

Graph 5.15

Wood manufacturers in Asia have a comparative advantage

It may seem odd that New Zealand is producing more wood but narrowing its hold on the value chain by choosing to export the logs as is, rather than adding further value domestically. However, this trend makes sense when one looks at the relative returns of forestry products on international markets.

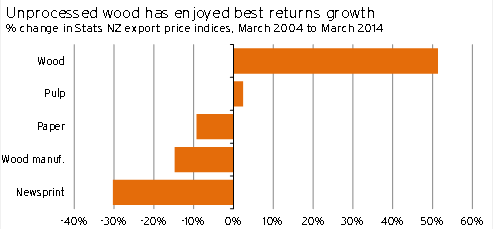

Over the ten years to March 2014, wood export prices (which includes logs) rose by 51%, while prices for manufactured wood and paper fell heavily (down 15% and 9% respectively).

Graph 5.16

The reality is that New Zealand has been unable to compete with the massive expansion of lower-cost, larger-scale forestry manufacturing capacity in China and Southeast Asia. This expansion has been supported by huge economies of scale, low wage costs, and state support from low fixed exchange rates and preferential loans from state-aligned banks. These factors are outside of New Zealand’s control, and we have had to take structural changes to the nature and location of global forestry manufacturing as given. In this way, by supplying raw inputs, New Zealand is just part of a broader supply chain.

In this environment, New Zealand’s forestry industry has increased its focus on the part of the supply chain where we maintain a comparative advantage – the actual growing of the trees for harvest. This advantage stems from our temperate climate, ample water resources, and availability of sufficient land for plantation forestry.

The forestry industry remains able to generate a good return from managing and harvesting plantation forests, in comparison to many players in the processing side of the industry, who have struggled to earn returns that justify the investment into capital.

What can be done?

In response to these struggles, many forestry manufacturers and processors have downsized or even closed, while many others have cried out for the government to intervene. These cries have so far fallen on deaf ears with the current National government. However, Labour has promised to intervene, should it be elected, by offering targeted tax sweeteners to the forestry manufacturing industry.

Although we feel for those in the industry who are struggling, we do not believe Labour’s policy response is in the best interests of the New Zealand economy. We have an inherent distrust for policies designed to artificially direct the flow of resources into industries outside of usual market signals, unless of course there is a compelling argument for market failure. These types of policies tend to lead to a less efficient allocation of resources in the economy and, as a result, weaken overall economic returns.

The forestry industry must accept its external environment as given and instead focus on factors within its control. A good place to start for the industry would be to look at the few timber processors and wood manufacturers who have bucked the trend and still performed reasonably well within such a challenging external environment. A key theme that emerges within this group of successful processors is that they are either vertically integrated enterprises or that they have secure long-term contracts with forest plantations for supply.

The advantage of these structures is that the processors can plan for the future, with the certainty of knowing they will have a consistent long-term supply of logs on commercial terms they are happy with. These contracts also open the door to better bank loan or equity funding arrangements, as banks and investors are more likely to stump up cash for new investments in plant and machinery if they are confident in the continuity of the enterprise.

However, unfortunately for forestry processors, securing long-term supply is no easy task. Finding willing counterparties for long-term supply contracts can be difficult, as some forestry managers prefer to time log price cycles in spot markets when harvesting their plantations. Furthermore, there are a significant number of small forestry plantations in New Zealand that are too small to offer consistent long-term supply options.

1 Estimates taken from Infometrics’ regional GDP model; 2014 figures to this level of industry disaggregation are not yet available.