Total tourist spend falls despite increased visitor arrivals

International visitor arrivals figures released last month show that inbound tourism is running at a record level. Over the year to July 2013, there were 2.65 million overseas visitor arrivals, 0.4% more than the previous record a year earlier when tourist numbers were boosted by the hosting of the Rugby World Cup.

However, despite this rising tide of foreign visitors, many tourism operators are still crying that times are tough. A quick glance through the recently released International Visitor Survey (IVS) shows that these complaints aren’t just idle whinging – a change in the composition of where tourists are coming from is having a profoundly negative effect on the underlying level of tourist spending in New Zealand and altering what they spend their money on.

According to the IVS, total expenditure in New Zealand by international visitors1 over the year to June 2013 was $5.49 billion, 1.3% less than the $5.57 billion spent by visitors the previous year (and significantly less than in 2008 when spending was pushing $6 billion per annum). Dissecting this result further shows that the fall in visitors’ total spend was caused by three factors:

1) an increase in the number of visitors who stay here for a short period of time (arrivals from Australia and China tend to fit this category)

2) a decrease in the number of visitors who stay for a prolonged period of holidaying (arrivals from nations such as the US and parts of Europe tend to fit this category)

3) more frugal daily spending patterns by tourists once they are in New Zealand.

The remainder of this article, examines these factors in turn, before focusing on issues affecting the outlook for business operators in the tourism sector.

More Chinese and Australian visitors

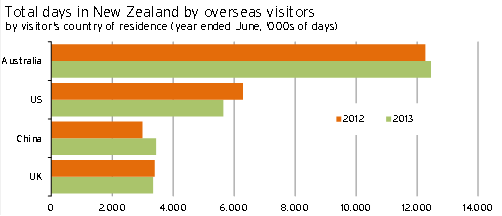

The composition of where tourists are coming from has changed significantly over the past five years. In the year to June 2008, visitor arrivals from our four biggest markets: Australia, the UK, the US, and China constituted 39%, 12%, 8.8%, and 5.0% respectively of total visitors to New Zealand. However, by June 2013, rapid growth in arrivals from Australia and China had pushed up their shares of visitors to 45% and 8.5% respectively, while the UK and US both saw their shares fall to 7.2%.

Visitors from these major markets stay for vastly different periods of time on average. The median length of stay for Australians (7 days) and Chinese (4 days) is far less than for visitors from the UK (20 days) and the US (9 days). Median stay lengths for visitors from Australia and the UK were unchanged from a year earlier, while over the past year median stays rose from 3 days to 4 days for Chinese visitors and fell from 10 days to 9 days for US tourists.

This changing composition of where visitors are coming from has reduced the total number of days spent in New Zealand by foreigners. According to the International Visitor Arrivals survey, overseas visitors spent 3.0% fewer days in New Zealand over the year to June 2013 than they had a year earlier, despite visitor arrival numbers rising to a record level. Graph 1 illustrates this change.

Graph 1

Furthermore, not only have total visitor days in New Zealand eased, but visitors have been displaying more frugal spending patterns once they are in New Zealand. The reasons for this spending restraint include: The strong New Zealand dollar eroding the value of budgets set in foreign currencies and more cautious attitudes to spending amidst a fragile global economic backdrop.

Over the past year, median daily spending has fallen across many of New Zealand’s key tourist markets. The median daily spend of Australian visitors fell 9.1%, while for UK visitors it fell by 19%. US visitors spent 11% more per day than a year earlier, but daily spending remains 9.2% below its level from the year to June 2010 when a stronger US dollar boosted American tourists’ purchasing power.

Although the median Chinese spend per day fell heavily (down 29% over the past year), their median spend per trip fell a more moderate 5.0%. It appears that Chinese travellers on package tours more or less fix a budget for their trip and so an increase in median stay length (from 3 to 4 days) simply meant that this budget was stretched more thinly.

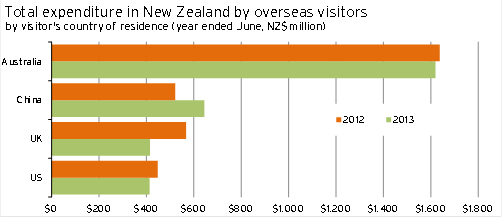

Combining this information on falling median daily spends with the data presented above on total days spent in New Zealand helps to explain why total expenditure by overseas visitors fell by 1.3% over the past year (see Graph 2). Of New Zealand’s key markets, only total spending by Chinese tourists increased, as a massive surge in arrivals from China more than offset any frugality in Chinese spending patterns.

Graph 2

What this means for tourism operators

This changing composition of visitor arrivals and spending patterns has been a double-edged sword for the tourism industry. Not only has the total volume of spending been under downward pressure, but the fact that visitors have been spending fewer days in New Zealand has left them with less time to visit more remote parts of the country.

At present, there are very few spots outside of Auckland and Queenstown/Wanaka to have seen international guest nights rise materially above their pre-Global Financial Crisis level. Even guest nights in Rotorua remain at a low level, as many Chinese tour groups choose to visit the region as a day trip from Auckland instead of overnighting. In most parts of the country, international guest nights remain 10% to 30% + below their pre-Global Financial Crisis levels.

With these trends in mind, it is not surprising that many tourist operators in regional New Zealand are doing it tough. The five years since the beginning of the Global Financial Crisis (GFC) have been extremely trying for tourist operators in regional New Zealand who cater towards longer-staying self-guided tourists from Europe and North America. However, once European and North American economies return to more normal health, there is no reason that arrivals from these parts of the world won’t recover to their pre-GFC level. This recovery will take some time, but at least those operators who have weathered the storm are leaner and more efficient than they were before the downturn and will be well poised to capture any pick-up.

On the other hand, tourism businesses fortunate enough to be exposed to the lift in arrivals from Australia and China have been enjoying permanent structural improvement. Cut-price air travel across the Tasman, as well as a growing number of New Zealand citizens residing in Australia coming home to visit family, are helping to boost arrivals from Australia. At the same time, inbound tourism from China has soared, as the rapid expansion of the Chinese middle class has increased demand for overseas travel to places like New Zealand.

But unfortunately, Chinese tourism has not been a golden ticket for all domestic tour operators. Even though visitor arrivals from China are continuing to grow rapidly, spending by Chinese tourists is still highly concentrated on a small subset of enterprises. This concentration of spending occurs because of the highly-structured nature and short duration of Chinese tours, coupled with anecdotal concerns regarding cronyism between Chinese tour operators and certain retail outlets.

At present, the majority of Chinese visitors arrive on group tours which only include New Zealand as a three or four-day add on to an Australia trip. These group tours are favoured due to a more streamlined visa process. However, if visas for independent travel are made more accessible then median stay lengths and, in turn, the range of regions which Chinese tourists visit and the activities they partake in will broaden.

Even so, to ensure they capture this increased custom, tourist businesses will still need to adopt new practices to satisfy Chinese visitors’ different cultural and linguistic background. I am not necessarily talking about reinventing the wheel, but following up a “kia ora” with a friendly “ni hao” would certainly be a good start!

Benje Patterson is an economist at Infometrics Ltd

1 Expenditure figures pertain to travelers aged 15+ and exclude international airfares.