Regions are more than one trick ponies

Sob stories of who has it worst in regional New Zealand were a popular topic for melancholic venters over recent years. But the chorus of complaint has subsided of late as evidence continues to emerge that most of our regions are actually performing pretty well at present. Despite the sky having fallen in on dairy for now, Infometrics’ latest Quarterly Economic Monitor has shown that our regional economies are far from one trick ponies, with improving fortunes in a number of other sectors propelling economic growth in most places along at healthy rates.

Let’s deal with the good for now, because frankly this article is unashamedly a good news story. I will deal with the bad briefly later in the article, but as you will see regions in this category are very much in the minority.

The good

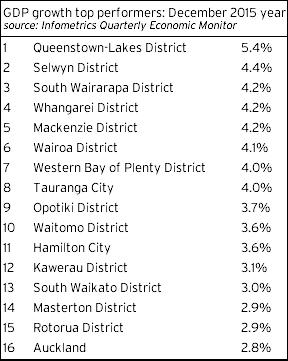

The table below identifies the top 15 performing territorial authorities over the year to December 2015 from a GDP growth perspective. For good measure, Auckland, in place number 16, has been tacked on the end for comparative purposes.

A quick scan through the list shows a couple of the usual regional stars, Queenstown-Lakes and Selwyn, up the top. But what is more interesting is looking further down the list and seeing the assortment of other top performers that follow. The majority of these top performers are dominated by urban and provincial territorial authorities in the upper North Island, as well as parts of the Wairarapa, Wairoa in rural Hawke’s Bay and bourgeoning tourism hotspot, Mackenzie District, in the South.

Who would have thought that a year or two ago we would have been labelling places like Kawerau and South Waikato as being “growth hotspots”?

This seemingly random assortment of top performers begs, the question of what is really going on in regional New Zealand at present? After all, with headlines continuing to dwell on dairy’s malaise, it seems pretty strange at first brush that even some key dairying areas in the upper North Island are performing well.

Back in September, I argued that it wouldn’t all be doom and gloom in regional New Zealand over the second half of 2015. I countered that there were areas with reasons for optimism that “…all have relatively low exposures to dairying and are selling goods and services whose returns have been boosted by the recent sharp falls in the New Zealand dollar”.

As it eventuates, my optimism for regional New Zealand, which was bucking the general sentiment floating around at the time, was still not optimistic enough. I was correct that other parts of the primary sector would pick up the slack, and that tourism would enjoy a golden summer, but I had underestimated just how strong these trends would be.

The values of pretty much every non-dairy primary sector export, including: honey, fruit, meat, wool, wine, vegetables, fish, and even forestry are back in growth mode, while arrivals of international visitors have accelerated to a double-digit rate of growth.

Furthermore, the spilling over of housing demand from Auckland’s increasingly unaffordable housing market into other parts of the upper North Island, as well as the positive demand stimulus from elevated inbound net international migration have been quite incredible to watch over recent months.

Our forecasting team had been taking into consideration the prospect of a more widespread housing market pick-up. However, we are still surprised to see just how widespread this growth has been, with house price inflation in pretty much all of the upper North Island running in the 10-25%pa range and house sales rising strongly. This increased turnover in the housing market and influx of migration is a key factor underpinning demand in upper North Island economies.

With migration inflows showing no signs of abating just yet, Auckland housing still expensive, and low interest rates helping keep the cost of servicing a mortgage at bay, this trend looks set to continue a while yet.

The bad

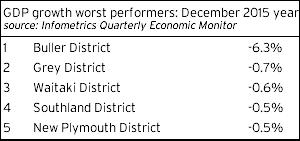

Having now dealt with the positives, I want to now quickly deal with what’s happening at the tail end of regional New Zealand. The table below identifies a short list of the five territorial authorities that suffered from a recession during 2015.

As would be expected, given such a prolonged and deep downturn in the dairy sector, the majority of these struggling provincial economies are places with high dairy exposures. The sharp downturn in oil and coal prices has also pulled down mining and exploration activity on the West Coast and in Taranaki.

It is likely that these areas will continue to face challenging times over the next couple of quarters, but there will be a few bright spots for some from parts of the agricultural sector where returns have risen, as well as further growth in tourist flows, particularly in the West Coast and Fiordland in Southland District.

Message of the day

The message that delving behind the numbers in Infometrics’ most recent Quarterly Economic Monitor has taught me is that it is important to not get too caught up in cyclical movements in one sector alone. Although dairying is a mainstay for many regions, there is much more to regional New Zealand than meets the eye. Rather than whining at what we don’t have, we should celebrate the success for those doing well.

Much of regional New Zealand is actually in a surprisingly good place at present, with the benefits of diversification in the primary sector showing through in many places. The willingness of New Zealanders to migrate regionally in search of affordable housing has also helped. Perhaps the lesson we should be learning from all this is that a diverse and flexible economy is a resilient one.